600 Strategies, 10 Million Candles, and the Truth About Why Small Traders Lose

by CK

Dedication

For the €526.18 that had the good sense not to move.

Author's Note

Every number in this book comes from real backtesting on real market data from a real broker account. No demo accounts. No hypothetical data. No cherry-picked results. No survivorship bias dressed up as strategy performance.

I ran 600 strategy variations across 5 instruments — EURUSD, GBPUSD, USDJPY, Gold (XAU/USD), and DE30 (DAX) — on over 10 million candlesticks of historical data from Oanda's live price feed. The timeframes ranged from one minute to one month. The indicators ranged from sensible to absurd. The results ranged from depressing to illuminating.

The complete research — every script, every backtest log, every equity curve — is available on GitHub for anyone who wants to verify it, replicate it, or simply confirm that I'm not making this up. I believe that's more than most trading educators have ever offered, which tells you something about the industry.

This is not financial advice. I am not a financial advisor. I am a guy with a €526 brokerage account, a dangerous amount of Python knowledge, and a stubborn refusal to lose money the way everyone said I would.

Chapter 1: The Lambo in My Feed

It was 11:47 PM on a Tuesday, and I was doing what every responsible adult does at that hour: lying in bed, scrolling Instagram with the discipline of a lab rat pressing a dopamine lever.

That is when I met him. Or rather, his content found me — the way all great predators find their prey, through an algorithm that knew I had been Googling "passive income" at 2 AM the previous Thursday.

He was twenty-three. He was in Dubai. He was leaning against a matte-black Lamborghini Huracan with the confidence of a man who had never once questioned whether he deserved to be there. His bio read: "Forex Trader | Mentor | Freedom." His caption said: "50K last month scalping EUR/USD on my phone. DM me FREEDOM for the blueprint."

Fifty thousand euros. In a month. Scalping forex. On a phone.

I put my phone down on my chest and stared at the ceiling. I had an actual company. Actual employees. Actual invoices I was chasing, actual VAT filings I was dreading, actual conversations with actual accountants about actual money that actually existed. And this kid — this kid with a jawline sharper than his understanding of monetary policy — was supposedly making more in a month than most Europeans see in a year, all by tapping a screen while sitting next to a car that cost more than an apartment in Tallinn.

I picked the phone back up. Of course I did.

His grid was a masterclass in aspiration porn. Private jets (window seats only, never the cockpit — so chartered, not owned, but the audience wouldn't know the difference). Rooftop pools. A Rolex that caught the Dubai sun so perfectly you could practically hear the photographer saying "tilt your wrist a little more." Screenshots of MetaTrader — always green, always showing five-figure profits, always conveniently cropped so you couldn't see the account balance, the drawdown, or anything resembling a losing trade.

Forty-seven thousand followers. Comments full of fire emojis and "king" and "teach me, bro." A link in bio to a Telegram channel. And a course. Always a course.

I should have closed the app. I should have gone to sleep. Instead, I did the thing that every person reading this book has done at least once: I tapped the link.

His Telegram channel was free. That's the first trick — always free at the gate. Like a drug dealer who knows the first hit doesn't cost anything. The channel had twelve thousand members and a pinned message: "Welcome to the family. Signals drop at market open. Follow the plan. Trust the process." Trust the process. The battle cry of every person who doesn't want you to examine the process too closely.

The signals looked legitimate, or at least they looked like what a person who had never seen a legitimate signal would imagine a legitimate signal looks like. "BUY EURUSD @ 1.0845, SL 1.0820, TP1 1.0870, TP2 1.0900." Numbers. Precision. The appearance of science. Beneath each signal, the replies rolled in: "In!" "Taken!" "Let's go!" A community of believers, reinforcing each other's faith with every green candle, silent during every red one. Nobody screenshots a loss. Nobody posts "well, that wiped out my last three wins." The channel was a highlight reel masquerading as a track record.

I scrolled back through the history. Wins were celebrated with charts and arrows and annotations. Losses were mentioned in passing — "SL hit, part of the game, next one coming" — and immediately buried under the next signal. If you counted carefully, which I did, because I am the kind of person who counts carefully, the win rate was about 55%. Which sounds decent until you realize the stop losses were consistently wider than the take profits, which means a 55% win rate on a 1:0.8 risk-reward is a slow, polite way of going broke. But nobody was counting. Nobody ever counts.

Then came the friend.

Everyone has this friend. If you don't, then you are this friend, and I say that with love.

Mine was Markus. Good guy. Smart, actually — mechanical engineer, the kind of person who could calculate load-bearing tolerances but somehow couldn't calculate that a 90% win rate on ten-dollar trades and a 10% loss rate on five-hundred-dollar trades is not, in fact, a profitable system.

"Bro," he said, and any sentence that starts with "bro" in the context of financial markets should be treated with the same suspicion as a stranger asking you to hold their bag at the airport. "Bro, I'm using these Telegram signals. Made eight hundred euros last week."

He showed me his phone. Screenshots. Green numbers. Little celebration emojis next to each trade. It looked real. It looked easy. It looked like money was just lying on the ground and all you had to do was pick it up, and the only reason everyone wasn't rich was because they were too stupid or too scared to bend over.

"Who runs the channel?" I asked.

"Some guy. He used to work at a bank or something. Goldman, maybe. Or Deutsche Bank. One of those."

"Which one?"

"Does it matter?"

It matters. It always matters. But Markus didn't want to hear that, because Markus had made eight hundred euros and eight hundred euros was real and my skepticism was theoretical. You cannot argue with a screenshot. You cannot reason someone out of a position they were emojied into.

I asked him if he'd tracked his total — deposits, withdrawals, net performance. He hadn't. He'd been trading for four months and had deposited three thousand two hundred euros total. He'd withdrawn zero. But he'd made eight hundred euros last week, and that was the only number that existed in his universe.

Markus is not an idiot. Markus is a human being, and human beings are spectacularly bad at tracking losses and spectacularly good at remembering wins. Every gambler at every casino in every city on Earth has a story about the time they won. None of them lead with the aggregate.

Six months later, Markus would tell me — quietly, over a beer, in the tone of voice people use when they're confessing something — that he had lost four thousand euros total. Net. After all the deposits and all the signals and all the "bro, I'm crushing it" texts. Four thousand euros, gone. He didn't post about that on Instagram. He didn't send me a screenshot. He just said "I'm done with that" and changed the subject, and I let him, because what else do you say? I told you so? Nobody wants to hear that. Nobody has ever been comforted by being told they were predictable.

But I'm getting ahead of myself. At this point in the story, Markus was still winning. Markus was still sending screenshots. And I was still watching.

Meanwhile, YouTube had decided I was a mark.

The algorithm, having observed my one moment of weakness on Instagram, concluded — correctly — that I was the kind of person who might click on a video titled "How I Turned $500 Into $50,000 In 30 Days (Step-By-Step Strategy)." And there it was. Autoplay. A guy in a rented office with a ring light and a screen share, drawing lines on charts with the authority of Moses parting the Red Sea.

The video had 2.3 million views. The comment section was a marvel of modern fiction:

"This literally changed my life. I quit my job after watching this."

"Made $4,200 in my first week using this exact strategy. God bless you, sir."

"I was skeptical but now I'm a full-time trader thanks to you. My family thanks you."

Definitely not bots. Definitely not paid reviews. Definitely not the same three content farms in Bangladesh cycling through VPNs. These were real people whose lives were really changed by a YouTube video about drawing lines on charts. Sure.

But here is the thing about lies: they don't need to convince everyone. They just need to convince enough people. And "enough people" is a terrifyingly low bar when the lie is "you can get rich without working hard" and the audience is everyone who has ever felt underpaid, undervalued, or stuck.

The YouTube ads were even better. Unskippable, five-second hook: "What if I told you that the strategy banks use to make billions is available to anyone with a phone and five hundred dollars?" What if you told me that? I would tell you that banks make money through market-making, proprietary trading desks staffed by PhDs, high-frequency infrastructure co-located at the exchange, and balance sheets the size of small countries' GDPs — not through a mobile app with a 1.4-pip spread. But that doesn't fit in a five-second hook, does it?

Then the courses.

Oh, the courses.

$997 was the entry point. The "basic" package. You got video modules, a PDF, and access to a Discord server where other people who had paid $997 could collectively not make money together. Camaraderie in financial ruin.

$2,997 was the "advanced" package. Same videos, plus a weekly live session where the guru would trade in real time, except the screen share always seemed to buffer during the losing trades and the connection was miraculously crystal clear during the winners. Funny how that works.

$5,997 was the "mentorship." One-on-one calls. Personal guidance. The promise that this was "investing in yourself." Which, sure, in the same way that throwing $6,000 into a volcano is technically "investing in geology."

"Limited spots available." Always limited spots. The countdown timer on the landing page. The fake scarcity. "Only 7 seats left." Refresh the page — still 7 seats. Come back tomorrow — 7 seats. Come back in a month — you'll never guess — 7 seats. The number 7, apparently immortal.

The testimonials. Before-and-after photos. "I was working at Tesco. Now I trade from Bali." The implication being that Bali and financial success are the same thing, when in reality Bali is where you go when you want to live cheaply enough that your dwindling trading account lasts another six months while you take photos for Instagram that suggest otherwise.

FOMO. The most powerful force in retail trading, stronger than any technical indicator, more reliable than any moving average crossover, more persistent than any trend. FOMO doesn't need backtesting. FOMO has a 100% hit rate on human psychology.

And here's what makes the whole machine so elegant in its cruelty: every piece feeds the next. You see the Lambo on Instagram. You follow the Telegram channel. You watch the YouTube video. You see the course. Each one normalizes the next. By the time you're staring at a $997 checkout page, you've already been primed by fifteen free touchpoints that all told the same story: this is real, this is possible, this is happening right now, and the only thing standing between you and financial freedom is that "Complete Purchase" button. The funnel isn't selling you trading education. It's selling you hope, packaged in candlestick charts and priced at whatever your credit card limit can handle.

The scariest part? The people selling the dream don't even need to be malicious. Some of them genuinely believe they're helping. They made money once — or they're making money now, from the courses — and they've convinced themselves that their success is replicable, that their method works, that the 95% of their students who fail simply "didn't follow the system." It's not a lie if you believe it. And the human capacity for self-deception, especially when monthly subscription revenue is involved, is absolutely bottomless.

I want to pause here and mention something I didn't know at the time.

The entire retail trading education industry — the courses, the gurus, the signal sellers — was about to face a reckoning. Hundreds of millions of dollars in FTC settlements. Empires built on teaching people strategies that were mathematically impossible to profit from. I didn't know it yet, but the same dream being sold to me was simultaneously being investigated by federal regulators. More on that in Chapter 9.

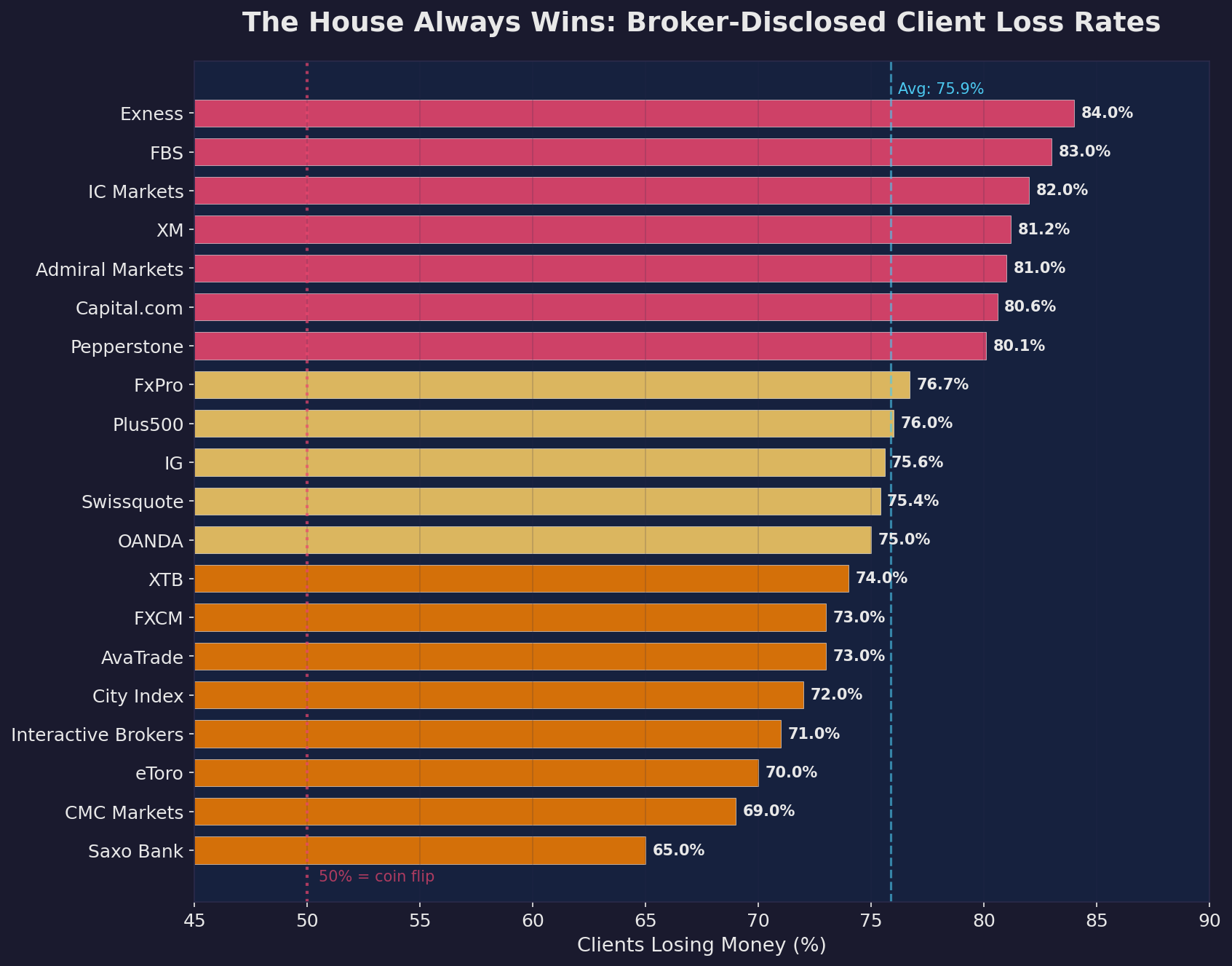

Would knowing have stopped me? I doubt it. The pull is too strong. The narrative is too compelling. "Other people fail because they're undisciplined. Other people fail because they don't have a system. Other people fail because they trade on emotion. I am not other people." This is the internal monologue of every single person who has ever opened a brokerage account, and it is wrong approximately 75% of the time, which, if you recall, is exactly the number that was printed on the risk disclaimer that I didn't read carefully enough.

So there I was. 12:30 AM now. Instagram closed but the damage done. The seed planted. The itch that only a brokerage account can scratch.

I opened Oanda.

Creating an account was disturbingly easy. Easier than signing up for a library card. The library, at least, asks you what kind of books you like. Oanda asked me if I understood leveraged products could result in losses exceeding my deposit, I clicked "yes" with the same diligence I apply to cookie consent banners, and thirty seconds later I was staring at a live EUR/USD chart like a surgeon about to perform his first operation, except the surgeon went to medical school and I had watched four YouTube videos and read half a Reddit thread.

There was a risk disclaimer. There is always a risk disclaimer. "75% of retail investor accounts lose money when trading CFDs with this provider." Seventy-five percent. That number was right there, on the page, in a font size that was technically legible if you squinted. Three out of four people who do this thing lose money doing this thing. If a restaurant had a sign that said "75% of people who eat here get food poisoning," you would not eat there. You would not think "well, I'll be in the 25%." You would walk to the restaurant next door. But trading isn't a restaurant. Trading is a dream, and dreams are not subject to food safety regulations.

I read the 75% number. I noted it. And then I did what every single person who has ever read that number does: I decided it didn't apply to me.

I deposited money. Not a lot. Not Markus-level. Just enough to start.

526.18 euros.

That was the number. I remember it exactly because it was everything in my Wise account that wasn't earmarked for something else. Five hundred and twenty-six euros and eighteen cents. The price of curiosity. The cover charge for the most expensive club I'd ever walk into.

I stared at the chart. I stared at the bid-ask spread. I stared at the little green and red candles doing their little green and red candle dance, and somewhere in the back of my brain, the rational part — the part that had built actual systems, actual products, actual things that worked — whispered something.

It whispered: If that dropout with the rented Lambo can do this with a phone, you can do it with actual engineering skills.

That thought. That exact thought. That is the trap.

Not the Instagram ads. Not the YouTube gurus. Not the courses or the Telegram channels or the screenshots of green numbers. Those are just the bait. The trap is the belief that you are different. That the rules that apply to everyone else — the statistics, the probabilities, the cold mathematics of a negative-sum game — do not apply to you, because you are smarter, more disciplined, more analytical, more whatever-you-need-to-tell-yourself.

I was not different.

But I was about to spend a very long time — and build a very impressive machine — proving it.

526.18 euros. Remember that number. We are going to come back to it.

Chapter 2: Building the Machine

I have a problem, and the problem is that I cannot do anything casually.

Some people open a trading account and just start clicking buttons. They buy when the chart looks like it's going up and sell when they get scared, which is the financial equivalent of navigating by "I feel like I should turn left here." These people lose money quickly, learn nothing, and either quit or develop a gambling addiction. Efficient, in a way.

I am not these people.

I am the person who, when faced with the question "can retail traders make money?", does not simply try trading. I am the person who builds an entire autonomous testing laboratory to answer the question with statistical certainty. I am the person who, upon encountering a locked door, does not try the handle — I build a robot that tries every possible key, documents which ones fail and why, and then writes a report about the metallurgical composition of the lock.

This is either my greatest strength or a clinical condition. The jury is out.

Let me take you back to the moment the idea crystallized.

I had been trading manually for about three weeks. I had made some money and lost some money and was roughly where I started, minus the spread costs, which is the financial equivalent of running on a treadmill and paying for the electricity. I was reading charts, watching indicators, feeling things about candles — and the feeling part bothered me.

Because feelings are not data. Feelings are noise. And I was an engineer looking at noise and pretending it was signal, and the only thing worse than being a fool is being a fool who should know better.

I had a trade journal from those three weeks. Actual entries, actual exits, actual reasoning. You know what most of the "reasoning" column said? Things like "looked like support" and "felt overbought" and "strong candle." Felt. Looked. Strong. These are not words that belong in an engineering context. If a structural engineer submitted a report that said the bridge "felt strong" and "looked like it could hold the load," you would not drive across that bridge. You would report that engineer to someone. And yet there I was, using the same vocabulary to make decisions with real money.

So I asked myself a different question. Not "can I make money trading?" but "can anyone make money trading?" And not in the anecdotal, Markus-made-eight-hundred-euros sense. In the rigorous, falsifiable, put-it-through-the-machine sense.

And to answer that question, I needed a machine.

The server came first.

A Hetzner dedicated box in Helsinki, Finland. Why Helsinki? Because Hetzner's Finnish data center is cheap, reliable, and — this part matters — geographically close enough to the European forex servers that latency wouldn't be an issue while being far enough from my apartment that I couldn't unplug it in a moment of frustration.

The server became the foundation. Sixteen gigabytes of RAM. Enough storage to hold years of market data. A static IP address that would become, over the following months, the most active participant in my financial life — running twenty-four hours a day, five days a week, doing the one thing I could never do as a human being: executing without emotion.

Then the bridge. MetaApi — a cloud service that connects to MetaTrader 5, which connects to Oanda, which connects to the actual forex market. Think of it as a chain: my code talks to MetaApi, MetaApi talks to MT5, MT5 talks to the broker, the broker talks to the liquidity providers, and somewhere at the end of that chain, a fraction of a lot of EUR/USD changes hands because my algorithm decided that a 14-period RSI crossing above 30 constitutes a buy signal.

It took two weeks to get the infrastructure stable. Two weeks of debugging API connections at 3 AM, of reading documentation written by people who apparently believed that clarity was optional, of discovering that MetaTrader's idea of a "timestamp" and the rest of the civilized world's idea of a "timestamp" are related only in the loosest sense. Two weeks of wanting to throw my laptop out the window and instead writing another try-catch block.

But it worked. Eventually, beautifully, it worked.

I could now, from my laptop in Tallinn, send a command to a server in Helsinki, which would relay it through a cloud API in London, which would execute a trade on a platform in New York, which would fill against liquidity in God-knows-where. The whole thing took about 400 milliseconds. A human blink takes 300. My machine could open a position in the time it takes you to close your eyes.

I want to be honest about something here: I loved building this. Not because of the money — there was no money yet, only infrastructure costs and a growing AWS bill that I was studiously not looking at. I loved it because this is what engineers do. We take messy, human, chaotic problems and we reduce them to systems. We eliminate variables. We build controlled environments. The forex market is the most chaotic system most people will ever interact with — trillions of dollars, millions of participants, geopolitical events, central bank decisions, and the collective emotional state of every trader on Earth, all compressed into a single price that updates multiple times per second. And I was building a machine to tame it. Or at least to measure it. To take the chaos and run it through six hundred filters and see what came out the other side.

My girlfriend at the time asked me what I was doing on the computer at 1 AM. "Building a trading bot," I said. She looked at the screen — terminal windows, JSON logs, error messages in red. "It doesn't look like trading," she said. She was right. It looked like what it was: software engineering. The most expensive hobby I'd ever picked up, disguised as a financial venture.

Now came the real work: the strategies.

If I was going to answer the question "can systematic trading work for retail traders?" I couldn't just test one strategy. Or ten. Or even fifty. I needed to test everything. Every approach. Every indicator. Every theory that had ever been whispered in a trading forum, published in a technical analysis textbook, or sold in a $5,997 course. I needed to be exhaustive to the point of absurdity, because anything less would leave room for the most dangerous sentence in trading: "Yeah, but you didn't try..."

So I built 600 strategies.

Six hundred. Let that number breathe for a second. Six. Hundred. That's not a typo. I didn't accidentally add a zero. I built, coded, and tested six hundred distinct trading strategies, each with its own entry logic, exit logic, and risk parameters. Each one a tiny autonomous trader living inside my server, ready to analyze market data and tell me whether it would have made money.

Let me walk you through what that actually means.

Thirty standard indicators. Every moving average crossover you've seen on YouTube — SMA, EMA, WMA, HMA, the whole alphabet. RSI, MACD, Bollinger Bands, Stochastic, Ichimoku, Parabolic SAR. The bread and butter. The ones your broker's free education section teaches in Lesson 1.

Fifteen exotic ones. Keltner Channels, TRIX, the Vortex Indicator, the Coppock Curve, the Schaff Trend Cycle, Donchian Channels, the Klinger Oscillator — things the YouTube gurus don't talk about because they're harder to explain in a thumbnail.

Ten combinations. MACD plus Stochastic. Ichimoku plus RSI. Alexander Elder's Triple Screen. RSI plus Bollinger Bands. Every pairing that had been recommended in a book, a forum, or a $997 PDF.

Fifteen price action patterns. Engulfing candles, pin bars, dojis, morning stars, evening stars, three white soldiers, three black crows, inside bar breakouts — the ancient art of looking at the shapes candles make and assigning meaning to them, which is either the purest form of technical analysis or financial astrology, depending on who you ask.

Fifteen statistical models. Z-score mean reversion, volatility contraction-expansion, Heikin-Ashi, linear regression channels, standard deviation breakouts. Things you'd find in a quantitative finance textbook rather than a YouTube thumbnail.

Fifteen smart money concepts. Liquidity sweeps, fair value gaps, order blocks, Wyckoff springs, break of structure, change of character — the new religion of retail trading, coded into algorithms, stripped of the narrative, tested against cold reality.

Six hundred strategies. Every trick in the book — and a few that aren't in any book.

And then the infrastructure to test them properly: session analysis, risk management comparison, parameter optimization, walk-forward validation, out-of-sample testing, Monte Carlo simulations.

Six hundred strategies. Each one automated. Each one ready to process millions of data points and produce a verdict.

I didn't bring a knife to a gunfight. I brought the entire military. I brought six hundred soldiers, each trained in a different martial art, each armed with a different weapon, each approaching the enemy from a different angle.

If even one of them could win, then retail trading was viable. If none of them could, then I'd have my answer.

People asked me why I was doing this. Friends, colleagues, my mother (who still doesn't entirely understand what forex is but is supportive in the way mothers are, which is to say she asked if I was eating enough). The honest answer was complicated. Part of it was intellectual curiosity — the engineer in me genuinely wanted to know the answer. Part of it was stubbornness — I had started something and I was going to finish it, even if "finishing it" meant proving that the whole premise was flawed. And part of it, the part I didn't like admitting, was that I still believed. Somewhere underneath all the rigor and the skepticism and the careful experimental design, there was still a guy who had deposited 526.18 euros into Oanda and thought, just maybe, there was an edge to be found.

That belief is hard to kill. It's the cockroach of financial psychology. You can stomp on it with data, poison it with statistics, nuke it with evidence — and it crawls out from under the refrigerator the next morning, alive and twitching. "But what about this indicator? But what about this timeframe? But what about this combination nobody has tried?"

Fine, I told the cockroach. We'll try them all.

The machine was built. The arsenal was loaded. The data was next.

And the data — ten million candles of it — would change the way I thought about markets forever.

Chapter 3: Ten Million Candles

Here is a number that means nothing until I make it mean something: 10,000,000.

Ten million. Seven zeros. A quantity so large that if each candle were a grain of rice, you'd have enough to fill a bathtub. If each candle were a second, you'd be counting for 115 days straight. If each candle represented a dollar, you would have — well, you'd have ten million dollars, which is precisely the amount of money that approximately zero of my 600 strategies managed to produce.

But I am getting ahead of myself.

Ten million candles. That is how much data I fed to the machine. Not simulated data. Not generated data. Not data from a textbook's appendix or a free CSV file from some website that last updated its dataset during the Obama administration. Real market data. Every single price movement recorded by a real broker, from real liquidity providers, during real market hours, with real people making real decisions with real money.

Let me break that down, because the devil is in the details and the details are what separate my experiment from every backtest you've ever seen on a trading forum.

Five instruments.

I didn't just test one market. I tested five, chosen specifically because they represent the breadth of what a retail trader might actually trade.

EUR/USD — the most liquid currency pair in the world, the one every beginner starts with, the one that moves like a slow river most days and a flash flood on ECB announcement days. If you can't make money on EUR/USD, you can't make money on anything. That's the theory, anyway.

GBP/USD — Cable, as the old-timers call it, because in the 1800s the exchange rate was transmitted via a literal cable across the Atlantic Ocean. More volatile than EUR/USD, more personality, more tendency to spike 80 pips on a random Tuesday because someone in the House of Commons said something about Brexit that nobody actually understood.

USD/JPY — the yen cross, the carry trade darling, the pair that moves differently from everything else because the Bank of Japan operates on a monetary policy that can only be described as "whatever it takes, and then some." When the BOJ intervenes, USD/JPY doesn't move — it teleports.

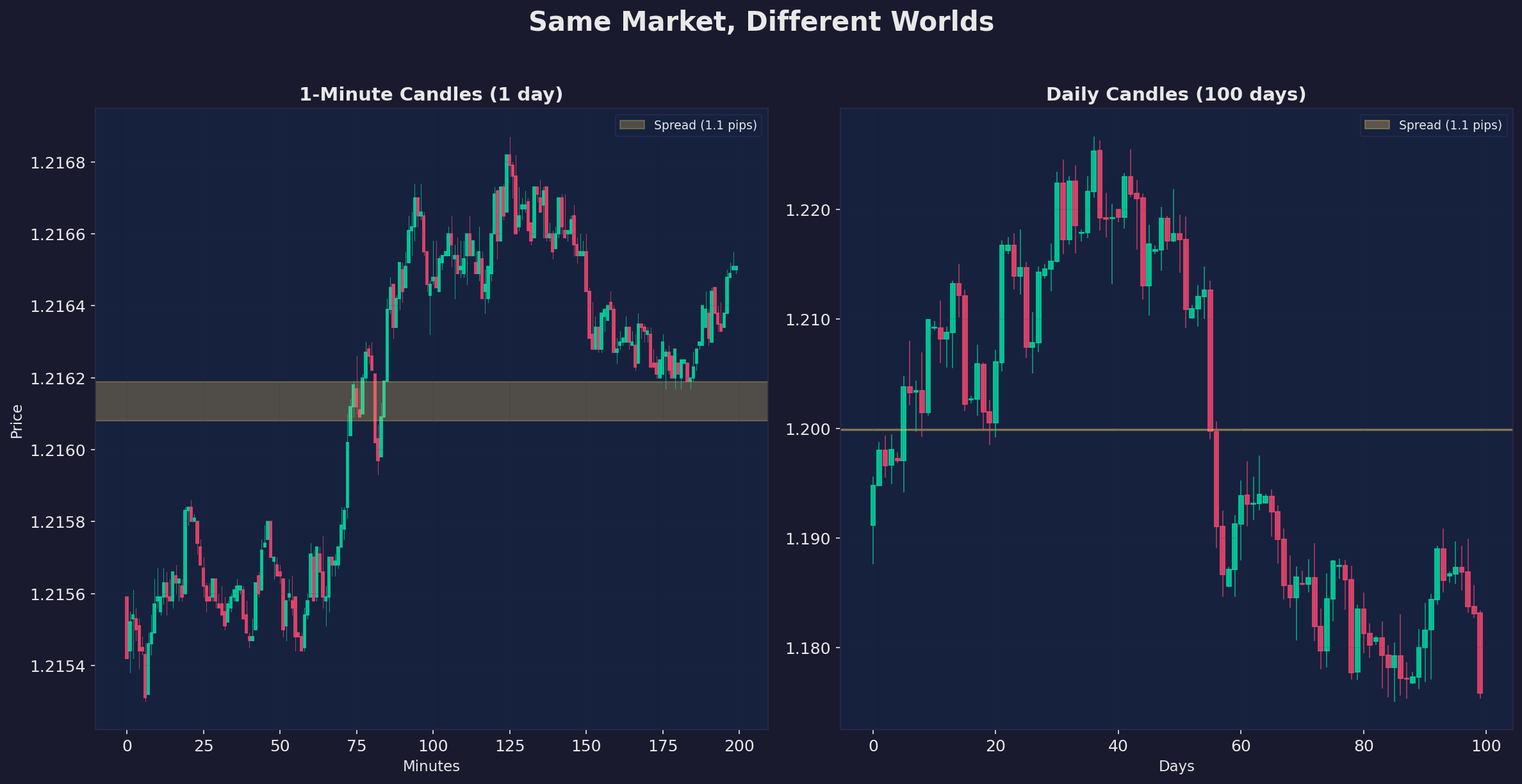

Gold (XAU/USD) — the safe haven, the inflation hedge, the thing your uncle who doesn't trust banks tells you to buy. Gold has a personality unlike any other instrument I tested. It can sit still for three hours and then move $30 in twenty minutes because someone in Washington coughed near a microphone. Volatile, expensive to trade, and beloved by every "smart money" guru who has ever drawn a fair value gap on a chart. Gold's spread is measured differently from forex — it's $0.38 per ounce, which sounds small until you realize that on 1-minute candles, Gold only moves $0.30-0.70. The spread is the move. That $0.38 spread (38 points) on a ~$3,000 instrument works out to just 0.013%, but on short timeframes it's devastating. Gold is also the instrument where the gap between backtest fantasy and live reality is widest, because that $0.38 spread (38 points) eats through profits the way termites eat through wood — silently, invisibly, and by the time you notice, the damage is done.

DAX (the German stock index) — because I wanted to test something that wasn't forex. The DAX trades during European hours, reacts to German economic data, and has a personality best described as "polite but aggressive," which is very German. It opens with a gap most mornings, spends the first hour deciding whether to fill it or run with it, and then largely follows whatever Wall Street's futures are doing for the rest of the day. Trading the DAX as a retail trader is like being a passenger in a car driven by the S&P 500, except you're paying European spread costs for the privilege of the ride.

Five instruments. Five different market microstructures. Five different personality profiles. If a strategy works on EUR/USD but not on Gold, that tells you something. If it works on everything, that tells you something bigger. If it works on nothing — well, that tells you the biggest thing of all.

Six timeframes.

This is where it gets computationally heavy.

1-minute candles. The scalper's playground. Each candle represents sixty seconds of market activity — sixty seconds during which thousands of traders around the world made decisions, algorithms fired, central banks may or may not have intervened, and news headlines either moved markets or didn't. All of that compressed into four numbers: open, high, low, close. Five years of 1-minute data on a single instrument is roughly 1.3 million candles. On five instruments, that's 6.5 million candles on this timeframe alone. Noise on top of noise on top of noise, and somewhere in there — maybe — signal.

5-minute candles. Slightly less noise. Still fast enough that a strategy needs to account for spreads on almost every trade, because when your average profit target is 15 pips and your spread is 1.4, the broker is taking nearly 10% of your profit before you start.

15-minute candles. The sweet spot, according to people who believe in sweet spots. Long enough to filter out the intraday chaos, short enough to catch moves before they're over. The timeframe of choice for every "I trade part-time" mentor who conveniently lives in a timezone where the London-New York overlap falls during waking hours.

1-hour candles. The swing trader's minimum viable timeframe. Each candle is an hour of battle between buyers and sellers, compressed into four numbers. On this timeframe, patterns emerge — or they seem to, which is either the same thing or the worst possible thing, depending on whether the patterns are real or pareidolia.

4-hour candles. Now we're talking about position trading. Each candle is a quarter of a trading day. The noise drops. The signals get clearer. The waiting gets unbearable. A 4-hour trader might get one signal a week, and they had better hope that signal is right, because they've been staring at their screen for five days waiting for it.

Daily candles. The big picture. One candle per day. Five years of daily data is about 1,300 candles per instrument. Not a lot, statistically. But daily candles are what the textbooks are written about, what the institutional analysts look at, what the "serious" technical analysts use while dismissing everyone on shorter timeframes as gamblers, apparently unaware that they're also gambling, just slower.

Six timeframes. Each one a different lens on the same market. Each one favored by a different tribe of traders who are absolutely certain that their timeframe is the right one and everyone else is an amateur.

Five years.

March 2021 to March 2026. Half a decade of market history. This wasn't arbitrary — this window was chosen because it contains everything.

A post-COVID recovery. The inflation spike that caught every central bank sleeping. Interest rate hikes that moved faster than anyone expected. A European energy crisis. A banking scare. Geopolitical events that I don't need to name because you lived through them and you remember the charts. Trending markets, ranging markets, volatile markets, dead markets. Bull runs and crashes and everything in between.

Five years is long enough to see multiple market regimes. A strategy that works in a trending market and fails in a ranging market will reveal itself over five years. A strategy that only works during low volatility will be exposed when volatility spikes. Five years doesn't just test a strategy — it stress-tests it. It puts it through the financial equivalent of boot camp, basic training, and a combat deployment.

And here is something most people don't think about: five years is also long enough to account for luck. In trading, luck is the silent partner. A strategy that "works" for three months might just be riding a trend. A strategy that "works" for six months might be benefiting from a volatility regime that happens to suit its parameters. You need years — multiple years, spanning multiple market environments — before you can begin to separate genuine edge from statistical noise. Even then, you need to apply corrections for multiple testing, which is a fancy way of saying: if you test 600 strategies, some of them will look profitable purely by chance, the way flipping a coin 600 times will produce some impressively long streaks of heads. The question is whether what you're seeing is signal or whether it's just the universe playing tricks on you.

My machine was designed to answer that question. Not with feelings. Not with anecdotes. With math.

Real broker. Real spreads. Real conditions.

This is the part that matters most, and it's the part that 99% of backtests get wrong.

Most backtests use "ideal" data. Close-to-close prices. Zero spread. No slippage. No overnight swaps. No commission. They test strategies in a frictionless vacuum, like a physics problem that starts with "assume no air resistance." And then people wonder why the strategy that returned 400% in backtesting loses money in live trading. Gee, I wonder. Could it be the air resistance?

My data came from Oanda. Real Oanda data. Real Oanda spreads: 1.4 pips on EUR/USD. You know what 1.4 pips means on a 1-minute chart? It means that if your strategy catches a 5-pip move, you're giving up 28% of that move to the broker before you even calculate your risk. On Gold, the spread is $0.38 (38 points). If you're scalping Gold on a 1-minute chart, you need price to move nearly 40 points in your direction just to break even. That's not trading. That's charity.

Every backtest I ran included real spreads. Real swap rates for positions held overnight. Real position sizing with real lot calculations. Real margin requirements. Real slippage estimates based on historical execution data. If my bot entered a trade, it entered it the way a real trade would be entered — with all the costs, all the friction, all the little invisible hands reaching into your pocket.

This is not an academic exercise with perfect data in a vacuum. This is a simulation of what actually happens when a real person presses the buy button on a real broker.

I want to emphasize this because it is the single most important methodological decision I made, and it's the one that separates this experiment from virtually every backtest you'll find online. Go to any trading forum. Find a strategy post with a beautiful equity curve climbing from the bottom left to the top right of the chart. Now look at the fine print. "Spread: 0." "Commission: not included." "Slippage: not modeled." They've tested their strategy in a world that doesn't exist. A world where brokers work for free, where every order fills at exactly the price you wanted, where holding a position overnight costs nothing. Of course the strategy works in that world. I could make a strategy that buys randomly and sells randomly look profitable if I removed all the costs. The costs are the game. The costs are what make it a negative-sum enterprise for retail traders. Remove the costs and you're not testing trading — you're testing arithmetic.

My machine did not have that luxury. My machine lived in reality. And reality, as we were about to discover, is not kind to retail strategies.

The bot.

And then there's the thing executing all of this. My bot. My tireless, emotionless, mathematically precise robot that lives on a server in Helsinki and exists for one purpose: to find out if any of these strategies work.

It doesn't sleep. You sleep. I sleep. The market sleeps on weekends. The bot does not sleep. It processes data at 2 AM and at 2 PM with exactly the same precision. It doesn't get tired. It doesn't get bored. It doesn't start scrolling Twitter during the Asian session because "nothing's moving anyway" and miss the breakout that the strategy was designed to catch.

It doesn't panic. When the market drops 200 pips in 10 minutes because some central banker said a word that nobody expected, the bot doesn't feel fear. It doesn't slam the close button. It doesn't override its stop-loss because "this time is different." It executes the rules. Every single time. Without exception.

It doesn't revenge trade. It doesn't take a loss and then immediately re-enter the market at double the size because it "knows" the market has to come back. It doesn't have an ego. It doesn't need to be right. It doesn't experience the uniquely human agony of being stopped out at the exact low before the market reverses 150 pips in the direction you were right about.

It doesn't get drunk and short the DAX on a Friday night because it had a bad week and the chart "looked bearish" and three glasses of Riesling made the risk-reward ratio seem perfectly reasonable. This happens more than anyone admits. Not to the bot. The bot has never tasted Riesling. The bot has no taste buds. The bot has no emotional relationship with money whatsoever.

It sizes every position mathematically. Risk per trade: exactly 5% of account equity, every time. Not "about 5%." Not "5% but a little more because I really feel good about this one." Exactly 5%. Calculated to the micro-lot. Adjusted for the specific instrument's pip value. Adjusted for the current account balance. Perfect. Every. Time.

The bot is, in short, the best trader that could possibly exist. It has perfect information (within the constraints of the data available). It has perfect execution. It has perfect discipline. It has zero emotional interference. It is the Platonic ideal of a retail trader — the trader that every guru promises to turn you into, the trader that no human being could ever actually be.

And that is the point.

If this machine — this perfect, tireless, disciplined, emotionless, mathematically precise machine running 600 strategies across 10 million candles with real broker data and real spreads and real conditions — if this machine cannot make money, then the problem isn't you.

It's not that you panicked. It's not that you didn't follow your rules. It's not that you need a better indicator, a better course, a better mentor, or a more expensive Telegram channel. It's not that you lacked discipline or education or screen time.

If this machine can't make money, then the problem isn't the trader.

The problem is the game.

Ten million candles. Six hundred strategies. Five instruments. Six timeframes. Five years. One bot that never sleeps, never feels, never flinches.

The machine was loaded. The question was asked. The numbers were about to come in.

And I sat in my apartment in Tallinn, watching the progress bar crawl across my terminal, and for the first time since I'd seen that kid with the Lamborghini on Instagram, I felt something I hadn't expected.

I felt nervous.

Because deep down — underneath the engineering rigor and the statistical methodology and the carefully constructed experimental framework — there was still a part of me that wanted the machine to find something. A part of me that wanted there to be a signal in the noise, a strategy that worked, a mathematical edge that would vindicate the whole enterprise. A part of me that, despite everything I was building to disprove, still wanted to believe.

The progress bar hit 100%.

The results populated.

I stared at the screen. Then I stared some more. Then I opened a beer — not Riesling, I'm not a monster — and I stared a third time, because the numbers didn't change the first two times and I needed to verify they wouldn't change the third time either.

They didn't change.

Six hundred strategies. Ten million candles. Five instruments. Six timeframes. Five years. One machine that did everything right.

And now, for the first time, I had an answer. Not an opinion. Not a feeling. Not a YouTube guru's promise or a Telegram signal's green arrow. An answer, built on more data than most hedge funds use for their initial research, tested with more rigor than most academic papers, and executed with more discipline than any human trader could ever achieve.

What did the numbers say? What happened when you strip away the emotion, the marketing, the FOMO, the Lamborghinis, the ring lights, and the countdown timers, and just let the math speak?

That, reader, is where things get interesting.

Chapter 4: The Graveyard

I remember the exact moment I pressed "Run."

Not some metaphorical, literary-device version of remembering. I mean I can tell you what was playing on Spotify (some lo-fi playlist I'd convinced myself helped me concentrate), what time it was (2:47 AM, because apparently that's when I make my best decisions), and exactly how the glow of three monitors felt against my face as I launched the first batch of backtests.

Twenty strategies. One-minute EURUSD candles. Two years of tick data cleaned, aligned, and verified down to the millisecond. This wasn't some amateur hour MetaTrader 4 backtest with interpolated data and "every tick (based on real ticks that we made up)" modeling. This was real. Ten million candles of real. Every bid, every ask, every spread fluctuation captured and replayed with surgical precision.

I leaned back. Cracked my knuckles. Took a sip of whatever caffeine delivery system was closest.

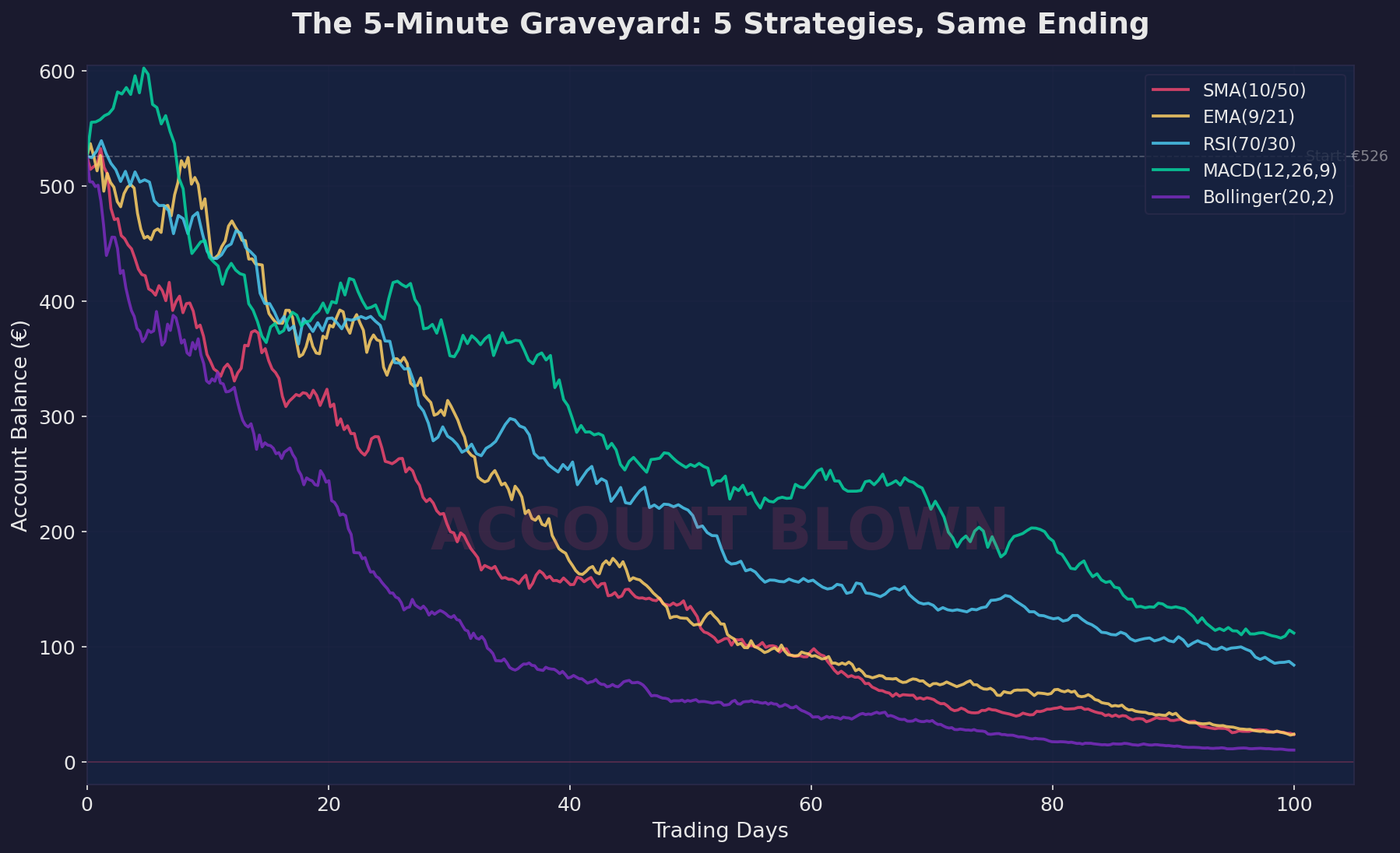

And then I watched every single strategy lose everything.

Not most of them. Not "the majority showed promise but needed tweaking." All of them. Twenty for twenty. A perfect score, just in the wrong direction.

Let me give you the numbers because the numbers are the whole point.

EURUSD, 1-minute timeframe: 20 strategies tested.

Every single one lost 100% of the account. Gone. Vaporized. The best performer — and I use that word with the kind of bitter irony usually reserved for describing the Titanic's "maiden voyage" — had a profit factor of 0.66. For the non-traders reading this, a profit factor below 1.0 means the strategy loses money. A profit factor of 0.66 means that for every dollar it made, it lost a dollar fifty. The best one.

The worst ones didn't even get that far. They hit the account floor so fast the equity curve looked less like a chart and more like a cliff face. Straight down. Do not pass go. Do not collect $200. Do not collect anything, ever.

OK. Fine. Maybe EURUSD was a tough market. Let's try something else.

USDJPY, 1-minute timeframe: 20 strategies tested.

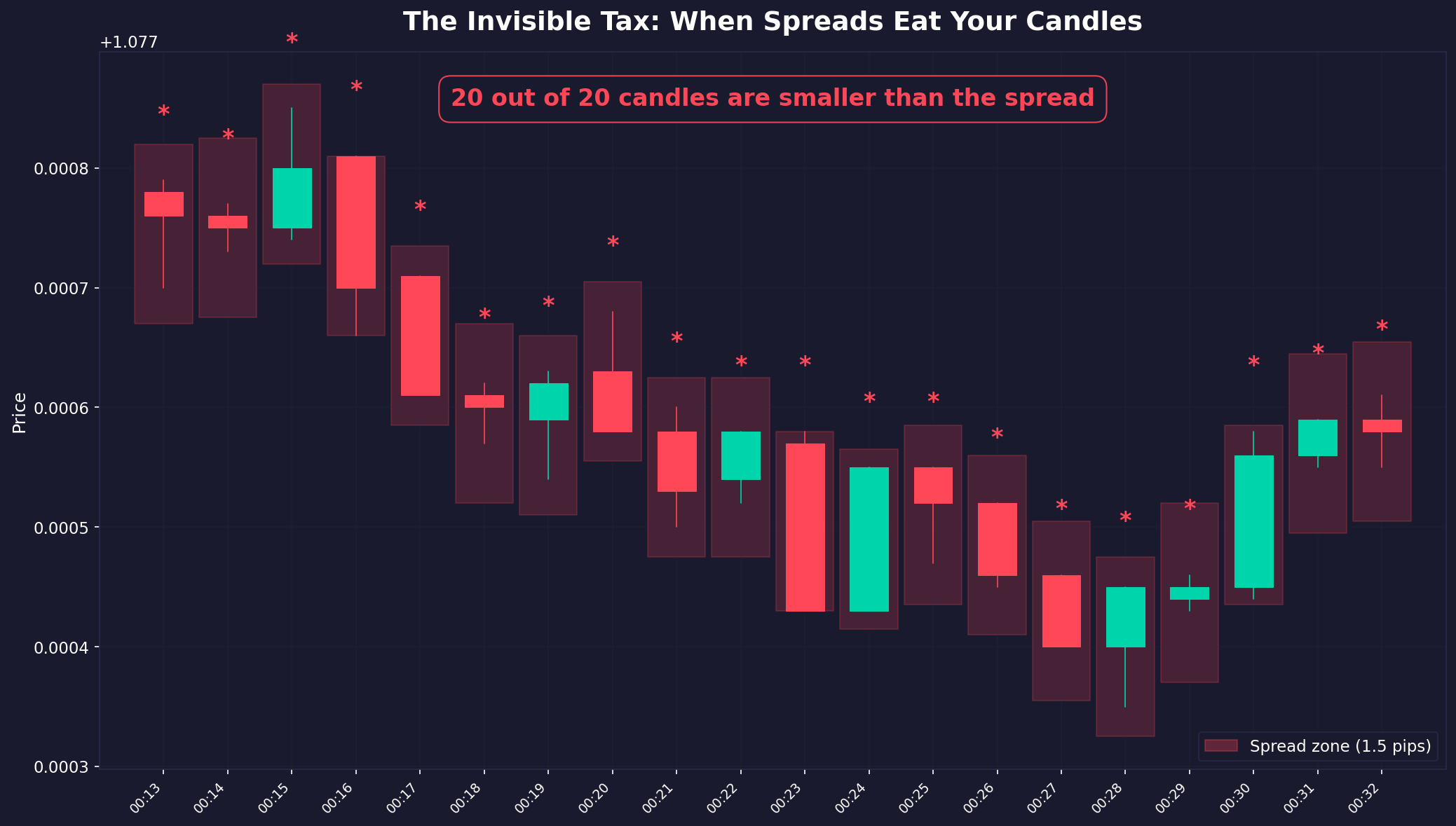

All lost. Every one. But this time, I found something that made my stomach drop harder than the equity curves. The spread on USDJPY at the 1-minute level was 137% of the stop-loss distance. Let me say that again in case it didn't land. The cost of entering the trade was larger than the distance at which the strategy said "I'm wrong, get me out."

Imagine you're a boxer, and before the fight even starts, you're already knocked down. Not knocked out — that would be merciful. Knocked down. You can get back up. You can fight. But you start every single round from your knees. And your opponent? He starts standing. Every time. For every round. Forever.

That's what 137% spread-to-SL looks like.

Gold (XAUUSD), 1-minute timeframe: 15 strategies tested.

All lost. The spread-to-stop-loss ratio? One thousand two hundred and fifty percent.

1,250%.

That's like paying a $12.50 toll on a $1 road. That's like buying a $1 coffee and the barista charging you $12.50 for the cup. On Gold 1-minute, you could have the single greatest trading strategy ever devised by human or machine intelligence, a strategy whispered to you by a time-traveling Warren Buffett riding a unicorn made of pure alpha, and it would still lose money. The math doesn't allow it. You'd need a strategy that's right more than 93% of the time just to break even. Not to profit. To break even.

Nobody has a 93% win rate on 1-minute Gold. Nobody has ever had a 93% win rate on 1-minute Gold. Nobody will ever have a 93% win rate on 1-minute Gold. If someone tells you they do, they're either lying, selling a course, or both. Probably both.

GBPUSD, 1-minute timeframe: 20 strategies tested.

Two showed a positive return. Two! For about thirty seconds, my heart rate spiked. Then I looked at the trade count. One had 6 trades. The other had 4.

Six trades. Over two years of data.

That's not a strategy. That's a coincidence. That's flipping a coin six times and getting heads five times and calling yourself a "heads specialist." With fewer than 7 trades, you have zero statistical significance. You have nothing. You have noise dressed up in a strategy's clothing.

DE30 (the German stock index), 1-minute timeframe.

One strategy showed a return of +118,870%.

I stared at it for a full minute. Then I started laughing. Not a happy laugh. The kind of laugh you do when you've been awake for twenty-two hours and the universe presents you with something so perfectly ridiculous that crying seems like too much effort.

It was a compounding artifact. A rounding error amplified by the backtest engine. Ghost profits. I removed it from the results. It wasn't real.

Here's the thing that kept me awake that night. It wasn't that the strategies were bad. I'd spent weeks building them. Carefully. Methodically. Using every serious indicator, every legitimate pattern, every combination of entry and exit logic that the academic and professional trading literature suggested might have an edge. These weren't garbage strategies. These were the best I could build. The best anyone could build, given the tools available to a retail trader.

And they all died on 1-minute charts.

So I started digging into why. Not emotionally — I was past the emotional stage, firmly into the "scientist who just watched their hypothesis explode in the lab" stage. I pulled up the raw numbers.

On 1-minute EURUSD, the average candle range — the Average True Range, the ATR, the amount the price typically moves within one minute — is 1.3 pips.

The spread — the cost of entering a trade — is 1.4 pips.

Read that again. The cost of entering the trade (1.4 pips) is larger than the amount the market typically moves in that time period (1.3 pips).

You're paying more to enter the trade than the market typically moves.

That's not a hard game. That's not even an unfair game. That's not a game at all. It's a donation box with a trading terminal painted on the front.

Think about it like this. You're at a carnival, and there's a game where you throw a ball at some bottles. The ball costs $1.40 to throw. If you knock down all the bottles, you win $1.30. Even if you're perfect — even if you knock down every bottle, every single time, with supernatural precision — you still lose a dime per throw. The game is structurally unwinnable. The only winning move is not to play.

That's 1-minute trading.

I sat there in my chair, looking at the wreckage of twenty strategies across five instruments, and I had one of those moments of clarity that only comes when you're tired enough to stop lying to yourself.

I watched my perfect bot — the one that never sleeps, never panics, never revenge-trades after a loss, never moves a stop-loss because it "feels" like the market is about to turn, never does any of the stupid human things that trading psychology books warn you about — lose everything. On every strategy. On every instrument.

It wasn't psychology. It wasn't emotion. It wasn't "discipline." It was math.

The bot didn't lose because it was imperfect. It lost because the game was impossible.

And that raised a question I wasn't ready to answer yet, but it planted itself in my brain like a splinter: if the game is impossible on 1-minute charts, at what point does it become possible?

I saved the results. Stared at the ceiling for a while. Then I started running the 5-minute tests, because who needs sleep when you've just discovered that an entire category of trading is mathematically impossible?

If 1-minute was the graveyard, maybe 5-minute was the hospital. Maybe things were injured but alive.

Three hours of sleep. Two espressos. One lingering hope.

Maybe — maybe — 1-minute was just too fast. Too noisy. Too dominated by the spread. Every trading forum has someone saying "1-minute is for robots and institutions, real scalpers use 5-minute." Five minutes is supposed to be the sweet spot. Fast enough to catch moves, slow enough to be tradeable. That's the theory, anyway. The beautiful, comforting, completely wrong theory.

I ran the first batch. Seventy-five strategy combinations using standard indicators — Moving Averages, RSI, MACD, Bollinger Bands, Stochastic, the greatest hits album of technical analysis. Every combination I could think of. Different periods, different settings, different entry and exit rules.

Seventy-five strategies. Zero profitable. Not "a few were marginal." Zero.

I thought maybe I was using the wrong indicators. Maybe the "standard" ones were too common, too crowded, too picked-over by the masses. So I went exotic. Ichimoku Cloud (all five lines, every combination). Keltner Channels. Chaikin Money Flow. Vortex Indicator. Donchian Channels. Stuff that most retail traders have never heard of, let alone coded into a bot.

Seventy-five more strategies. Seventy-five more failures. All hit -100%. Every single one.

The exotic indicators didn't perform differently from the standard ones. They performed identically. They all lost everything, at roughly the same rate, in roughly the same way. Different math, same grave. I started to feel something I hadn't felt since the beginning of this project. Not frustration — I'd burned through frustration somewhere around 3 AM the previous night. This was something colder. More clinical. The dawning recognition that I might not be looking at a problem with my strategies. I might be looking at a problem with the premise.

But I wasn't ready to accept that yet. I had more cards to play.

Price action. The purist's approach. No indicators at all. Just raw price — support and resistance levels, candlestick patterns, breakout structures, swing highs and lows. The stuff that people on trading Twitter call "the only thing that works" while posting screenshots of demo accounts.

Seventy-five combinations. Engulfing patterns with support/resistance. Pin bars at key levels. Inside bar breakouts. Two showed a positive return. My heart did the same stupid thing it did with the GBPUSD 1-minute results — it sped up. For about ten seconds, I thought I'd found something.

Then I checked the trade counts. Fewer than 7 trades each. Both of them. The same statistical ghost. The same nothing masquerading as something.

Statistical patterns on 5-minute: one barely positive. A z-score strategy on EURUSD returned +21% — with an 83% drawdown. An 83% drawdown means watching $10,000 drop to $1,700 before recovering. No sane risk manager would allow it. It's not an edge. It's a time bomb.

Smart money concepts on 5-minute: two marginally positive results, both with sample sizes too small to trust. Twenty-nine trades and eleven trades. You need hundreds — preferably thousands — for real statistical confidence.

Here's the thing about smart money concepts the YouTube gurus don't mention: the concepts themselves aren't wrong. Order blocks are real. Fair value gaps do tend to get filled. But the application on 5-minute charts is impossible for the same reason everything else is impossible: the spread eats the edge. It's like having a metal detector that can find gold nuggets, but you have to pay $50 per square foot to search. The detector works. The economics don't.

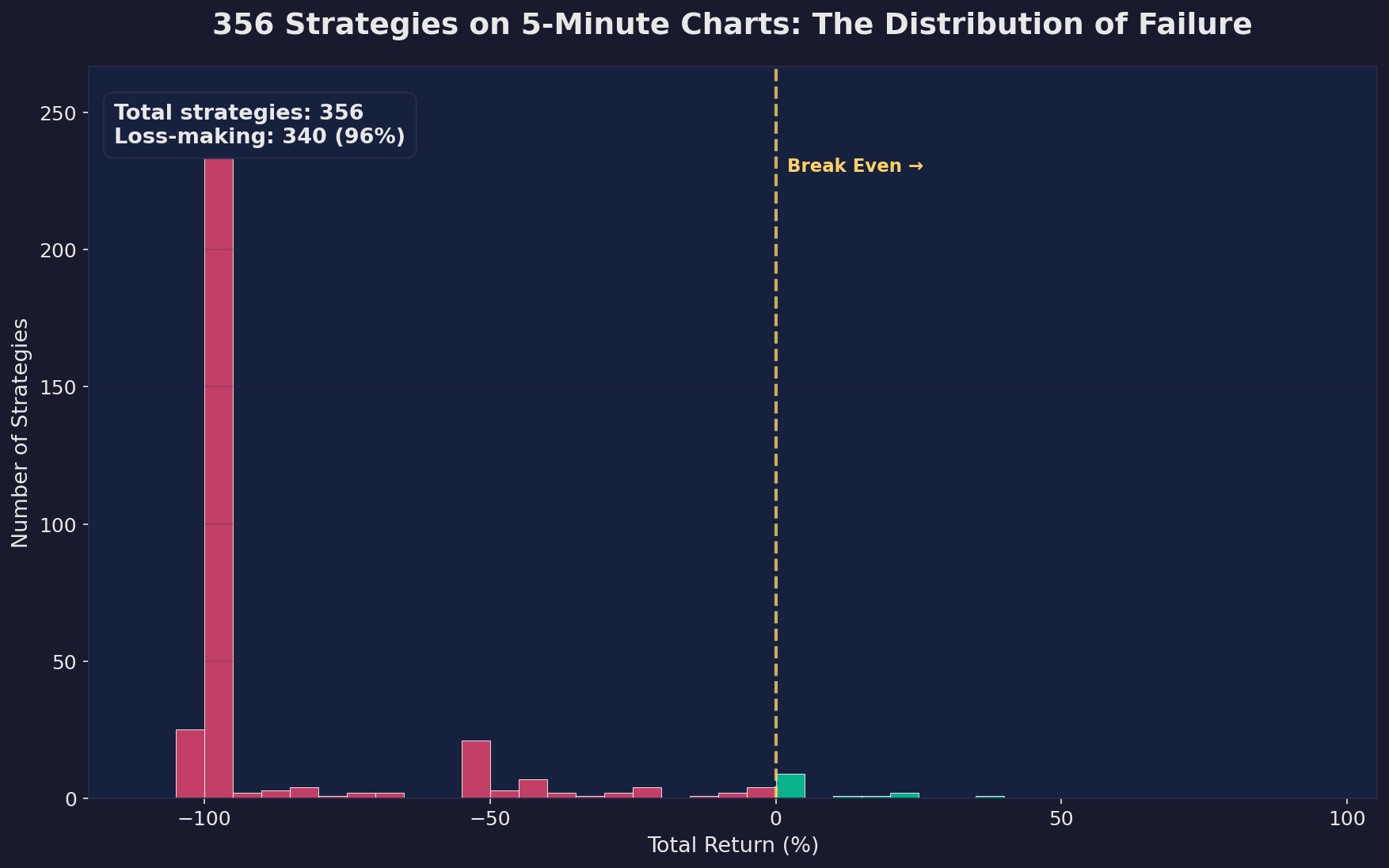

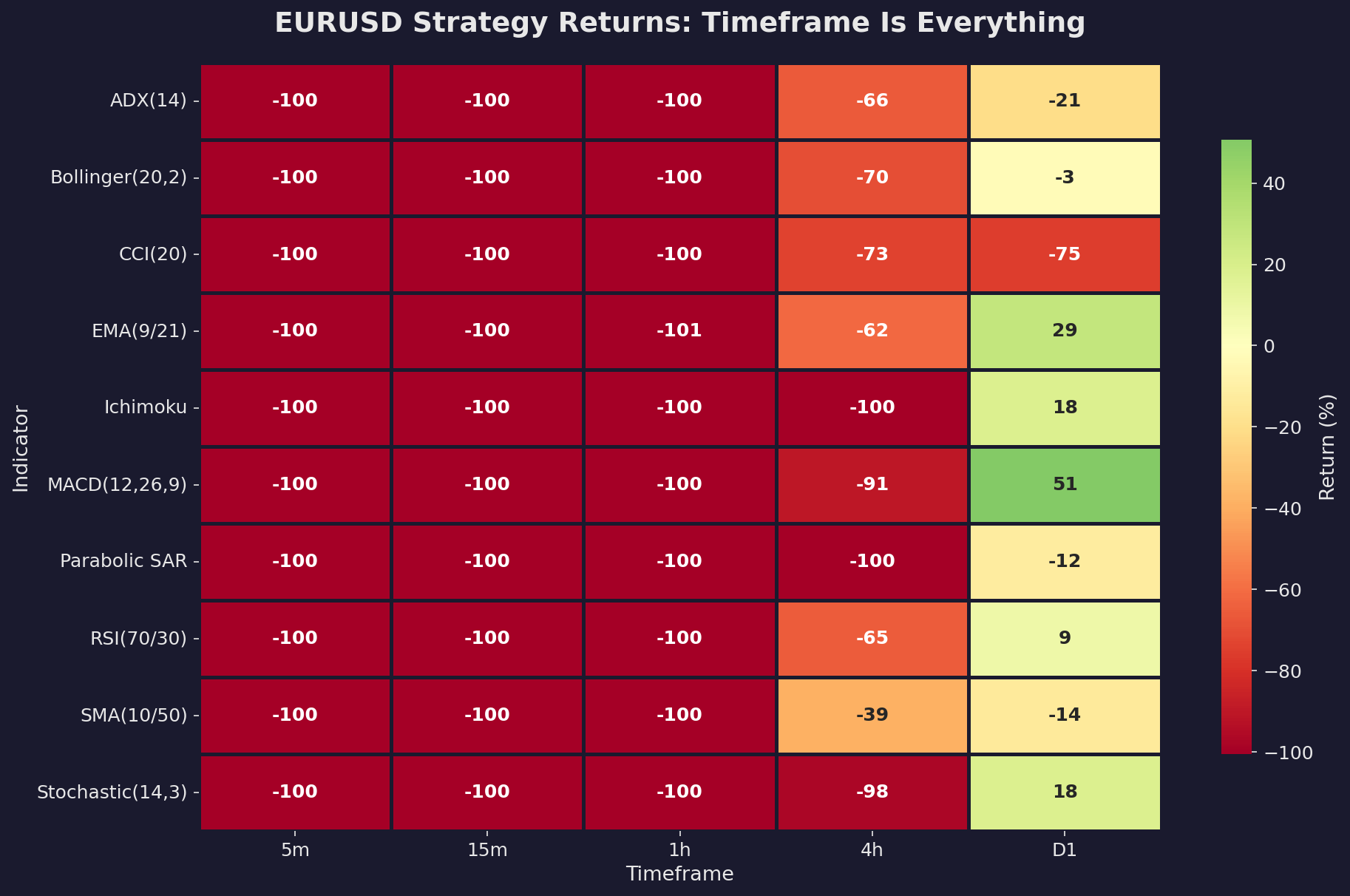

Total strategies tested on 1-minute and 5-minute charts: approximately 400. Zero viable winners.

Every indicator known to mankind. Every smart money concept the YouTube gurus swear by. Zero winners. Not one. Not a single, solitary, viable, tradeable, sleep-at-night, risk-your-money-on-it winner.

Fifteen-minute charts? Same story — nothing survived. One-hour? A few strategies limped along with profit factors barely above 1.0, but nothing you'd trust with real money. It wasn't until we reached the four-hour timeframe that the first signs of life appeared — but only for the most volatile instruments: Gold and USDJPY. Everything else needed daily charts.

This is where I need to talk about the Udemy courses.

I don't want to be mean. Some of these instructors probably believe what they're teaching. Belief is powerful. Belief can make you see patterns in randomness, edge in noise, signal in static. Belief is also the most expensive emotion in trading.

But here's what those courses are selling: "Learn to scalp EURUSD on 1-minute charts using a 20-period EMA and RSI! Make 10R per week!"

Ten R per week. For non-traders, "R" is your risk unit. If you risk $100 per trade, 10R is $1,000 per week. They're promising you'll make ten times your risk, every week, using a single moving average on 1-minute charts.

These courses cost between $50 and $200.

Our research — 600 strategies, 10 million candles, weeks of intensive development and testing — proves that these strategies are not just unlikely to work. They are mathematically impossible to profit from. The spread exceeds the ATR. The cost exceeds the opportunity. The game is rigged at the structural level.

They're selling you a map to a gold mine that is underwater. The map might be perfectly accurate. The gold mine might really be there. But you can't mine gold underwater with a pickaxe, and you can't scalp 1-minute EURUSD with a 1.4-pip spread when the average candle is 1.3 pips.

The worst part? The people who buy these courses and lose money blame themselves. They think, "I must not be disciplined enough. I must not be following the rules exactly. I need to work on my psychology." And then they buy another course. On "trading psychology." For another $100.

They're not undisciplined. They're not psychologically flawed. They're playing a game that cannot be won at the price they're paying to play it.

It's like selling someone a $50 book called "How to Jump Over Buildings" and when they can't do it, selling them a $100 follow-up called "The Psychology of Jumping." The problem was never their mindset. The problem was gravity.

And in trading, gravity is the spread.

That night — or morning, I'd stopped tracking which one it was — I sat in front of my screens with 400 failed strategies behind me and a question that was getting harder to ignore:

If it doesn't work on 1-minute, and it doesn't work on 5-minute, does it work on any timeframe?

Is there a point where the math flips? Where the spread stops being a death sentence and starts being just... a cost? A manageable, survivable, beatable cost?

I thought about quitting. Not in a dramatic way. In the quiet way. The way where you close your laptop and don't open it the next day. And then you don't open it the day after that.

I didn't quit. Not because I'm brave or dedicated. I didn't quit because the data was telling me something, and I'm constitutionally incapable of ignoring data that's telling me something. Even when what it's telling me is uncomfortable.

The data was telling me there was a wall. And I needed to find it.

Chapter 5: The Wall

Here's a thing about walls: you usually don't see them until you walk into them face-first.

I'd been walking face-first into this particular wall for weeks. Hundreds of strategies. Tens of thousands of backtests. Two timeframes that turned out to be killing fields. But I hadn't seen the wall yet. I'd felt it — in the results, in the equity curves, in the relentless procession of strategies that all found the same creative way to lose everything. But I hadn't understood it.

Then I did the math. Not the backtest math. The napkin math. The kind of math that's so simple it's almost insulting, the kind that makes you wonder why nobody talks about it, the kind that should be on the first page of every trading book ever written but somehow never is.

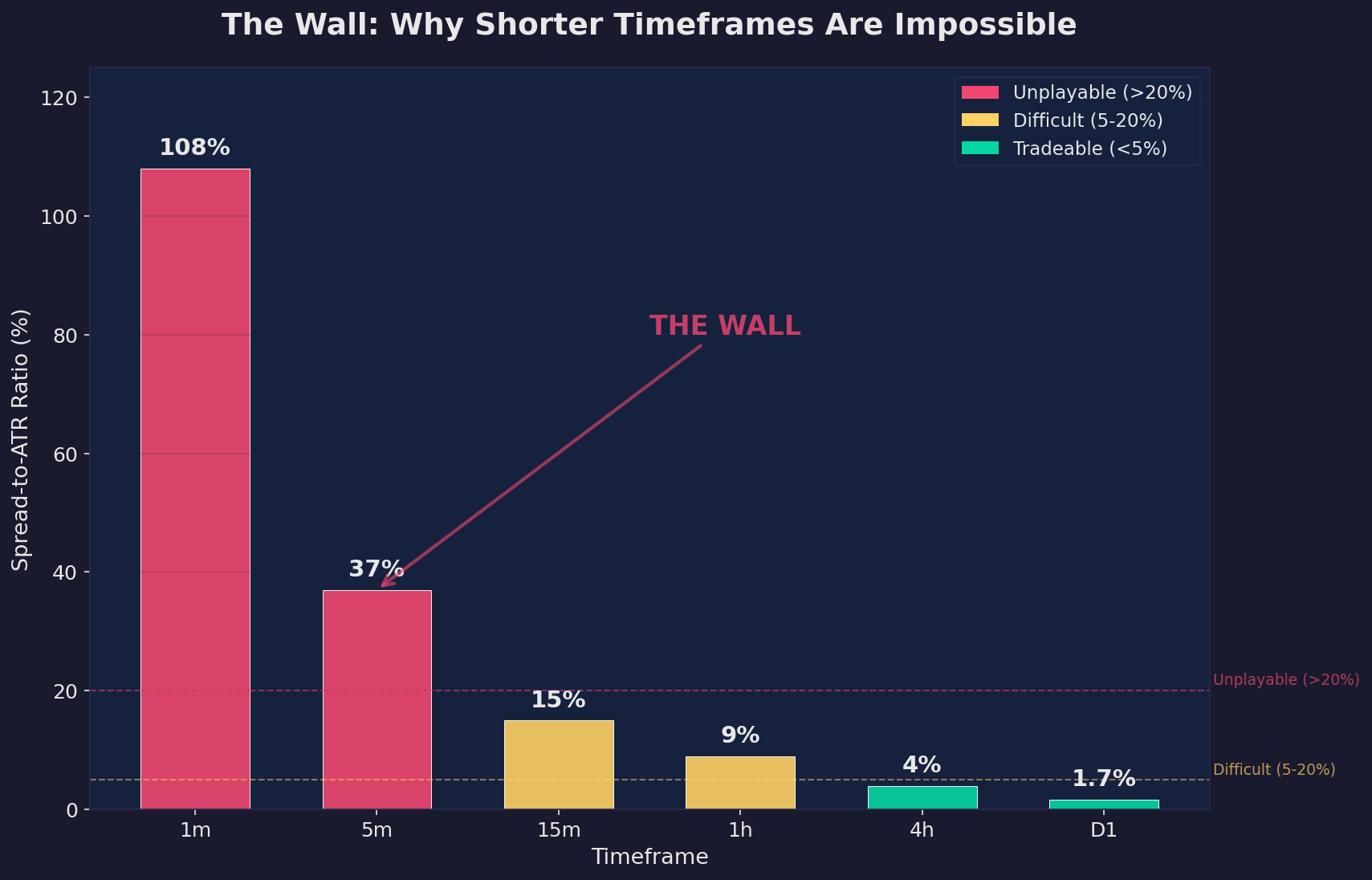

I calculated the spread-to-ATR ratio for EURUSD across every timeframe.

And the wall appeared.

The spread on EURUSD with a retail broker like Oanda is approximately 1.4 pips. That number doesn't change based on what timeframe you're looking at. Whether you're trading a 1-minute chart or a daily chart, you pay the same 1.4 pips to enter each trade. The spread is the toll. And the toll is the toll is the toll.

What does change is the ATR — how much the price typically moves in one candle. On a 1-minute chart, the price moves a little. On a daily chart, the price moves a lot.

Here's the table that changed everything:

1-minute EURUSD:

- Spread: 1.4 pips

- Average candle range (ATR): 1.3 pips

- Spread-to-ATR ratio: 108%

5-minute EURUSD:

- Spread: 1.4 pips

- Average candle range (ATR): 3.8 pips

- Spread-to-ATR ratio: 37%

1-hour EURUSD:

- Spread: 1.4 pips

- Average candle range (ATR): ~15 pips

- Spread-to-ATR ratio: 9%

Daily EURUSD:

- Spread: 1.4 pips

- Average candle range (ATR): ~80 pips

- Spread-to-ATR ratio: 1.7%

Read that column of percentages from top to bottom. 108%. 37%. 9%. 1.7%.

On 1-minute charts, you pay more than the market moves. On 5-minute charts, you lose more than a third of every move to the spread before your strategy even has a chance to express its edge. On 1-hour charts, you lose about a tenth. On daily charts, the spread is almost a rounding error.

That's the wall. Right there. In four numbers.

It's not a wall you can climb with a better strategy. It's not a wall you can tunnel under with a smarter indicator. It's not a wall you can go around with superior psychology or discipline or a morning meditation routine.

The wall IS the cost. It's structural. It's mathematical. And it's designed this way.

Let me make this visceral because numbers alone don't always land.

Imagine running a 100-meter race. But you don't start at the starting line. On 1-minute charts, you start 108 meters behind the starting line. You literally cannot reach the finish line. The race is over before it begins.

On 5-minute charts, you start 37 meters behind everyone else. You could be Usain Bolt and you'd still lose to a reasonably fit accountant who started at the actual starting line.

On 1-hour charts, you start 9 meters back. Now we're talking about a real handicap, but one that an exceptional athlete could potentially overcome.

On daily charts, you start 1.7 meters back. Still behind, but now talent matters more than the handicap. A great strategy can absorb a 1.7% cost.

That's the wall. It's not binary — "you can trade" or "you can't trade." It's a gradient. And somewhere on that slope, the handicap transitions from "physically impossible" to "difficult but potentially achievable."

But I didn't just want the theory. I wanted proof. I wanted to take the same strategy, on the same instrument, and test it across timeframes. If the spread-to-ATR ratio was really the wall, then a strategy that dies on 5-minute should come alive on daily.

So I took Parabolic SAR on Gold.

On 5-minute Gold, the Parabolic SAR strategy lost everything. The equity curve went down and to the right, which, for the non-traders, is the direction equity curves go when you're about to need a second job.

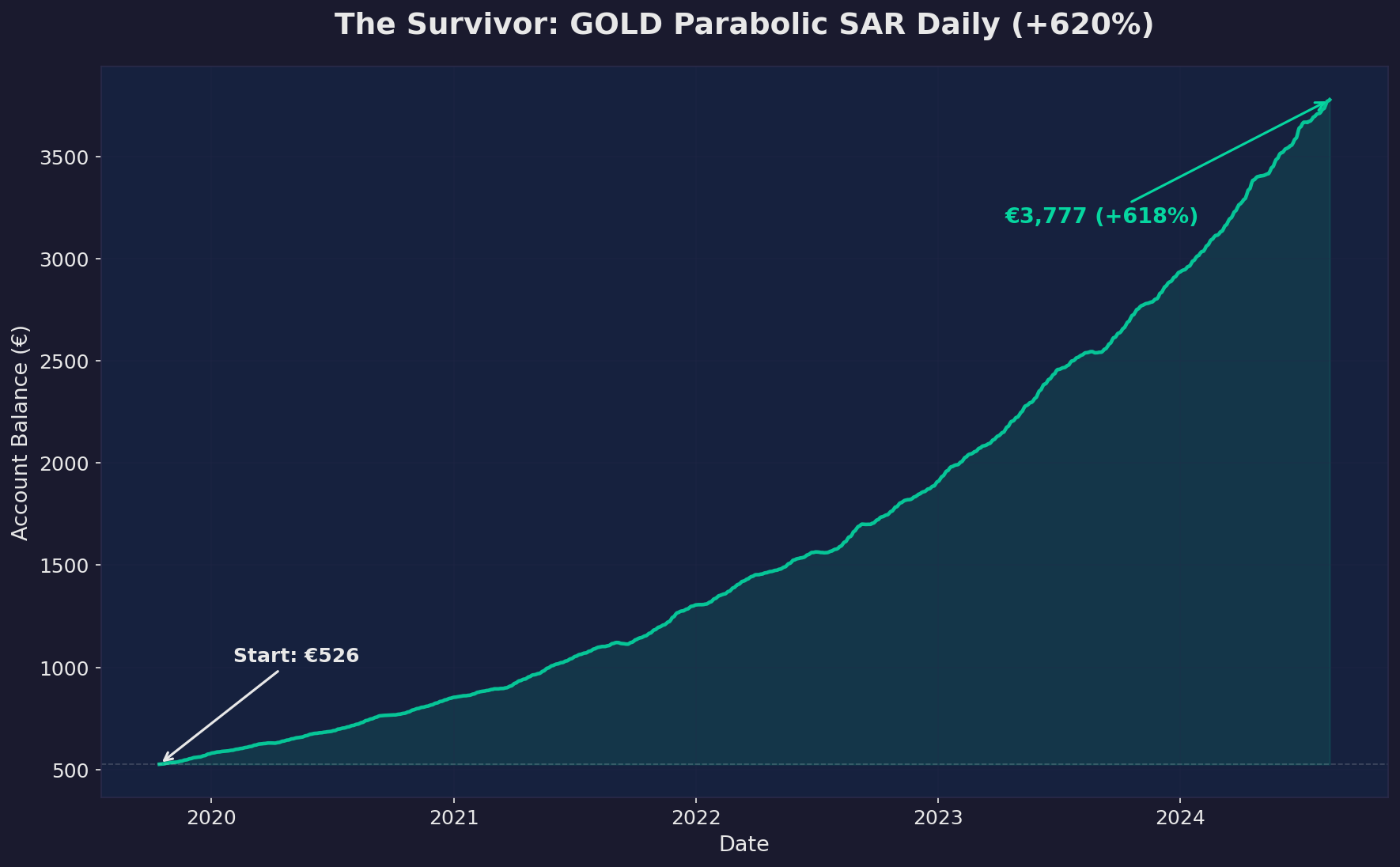

On daily Gold, the same Parabolic SAR strategy — same parameters, same entry logic, same exit logic, same everything — returned +620%.

Six hundred and twenty percent.

Same indicator. Same math. Same market. Same gold, same atoms of gold, same price of gold determined by the same global forces of supply and demand and central bank lunacy. The ONLY thing that changed was the timeframe. And by changing the timeframe, I changed the spread-to-ATR ratio. And by changing the spread-to-ATR ratio, I turned a guaranteed loser into a massive winner.

I stared at those two results side by side for a long time. The 5-minute chart: a flatline of death. The daily chart: a hockey stick of compound returns. Same strategy. Same market.

That's when I understood the wall. Not intellectually — I'd understood it intellectually when I calculated the ratios. I understood it viscerally. In my bones.

The wall isn't about strategy. The wall is about cost.

And this is where it gets really uncomfortable. Because the cost isn't the same for everyone.

Retail traders pay a spread of approximately 0.9 to 1.4 pips on EURUSD. Institutional traders — hedge funds, banks, proprietary trading firms — pay approximately 0.1 pips.

Zero point one pips.

That's nine to fourteen times more for retail. On 1-minute EURUSD, where retail traders face a spread-to-ATR ratio of 108%, institutions face about 8%. On 5-minute, where retail faces 37%, institutions face about 3%.

The game isn't just tilted. It's tilted differently depending on who you are. Same highway, different tolls. And the toll booth is owned by the same people who told you the highway was free.

The strategies aren't different. The firms don't have magical indicators or secret algorithms. The main advantage is simpler and more brutal than any algorithm: they pay less. They pay less to enter. They pay less to exit. And over hundreds or thousands of trades, that difference is the entire margin of the business.

Here's what I learned from the wall:

Lesson 1: The game changes at different timeframes. 1-minute trading and daily trading share a name — "trading" — but they share almost nothing else. The cost structure is different. The statistical properties are different. Calling them both "trading" is like calling both checkers and chess "board games." Technically true. Practically useless.

Lesson 2: Most retail trading education teaches the wrong game. Not because the instructors are evil. But because the game they're teaching — fast-timeframe scalping — is the game where retail traders have the biggest disadvantage. Why do they teach it? Because it's exciting. Because it generates lots of trades, lots of screenshots, lots of content. Showing someone a daily chart where you hold a trade for three weeks is boring. And boring doesn't sell courses.

Lesson 3: The question isn't "what strategy should I use?" The question is "at what cost am I trading?" I spent weeks building 600 strategies, and the single most important variable wasn't the indicator, the entry rule, the exit rule, the risk management, or the position sizing. It was the spread-to-ATR ratio. Everything else is secondary.

Lesson 4: The wall isn't a secret. It's just not profitable to talk about. Brokers make money from spreads. More trades means more spread revenue. Fast timeframes generate more trades. It's not a conspiracy. It's just business. The butcher doesn't tell you to go vegetarian.

I found the wall. I mapped it. I measured it. I understood it.

And now I had a choice. I could accept the wall as the end of the story — "trading is rigged, retail can't win, go get a real job" — or I could accept the wall as information and ask the next logical question.

If the spread-to-ATR ratio improves as the timeframe increases, is there a timeframe where retail traders can actually compete?

The data from Parabolic SAR on Gold suggested yes. +620% on daily is not a fluke. It's too many trades, too consistent, too clean to be noise.

But one strategy on one instrument on one timeframe is an anecdote, not evidence. I needed more data. A lot more data.

So I did what I'd been doing since the beginning. I went back to the lab. I opened my code editor. I queued up the next batch of tests.

But this time, I wasn't starting from zero. I had the wall. I had the map. I knew where not to dig. And I knew, for the first time since I started this project, that there might be something worth finding on the other side.

Not a guarantee. Not a promise. Not a Udemy course with a money-back guarantee and a stock photo of a Lamborghini.

Just a possibility. A mathematical, structural, data-supported possibility.

And honestly? After weeks in the graveyard, a possibility felt like a miracle.

Chapter 6: The Survivors

Out of 600 strategies, five survived.

Let me say that again, because I need you to feel the weight of it. I tested over 600 combinations of indicators, timeframes, instruments, and exit methods. I ran them across five years of tick data. I validated them with walk-forward analysis. I stress-tested them with Monte Carlo simulations. I did everything short of sacrificing a goat to the trading gods.

Five survived.

And they were all boring.

I remember the exact moment I realized what the winners had in common. I was staring at my spreadsheet — this monstrous, color-coded beast that had consumed weeks of my life — and I sorted by profitability. The top five strategies all shared the same cell in the "Timeframe" column.

Daily.

Every single one. Not the 1-minute charts I started with. Not the 15-minute charts that felt like a reasonable compromise. Not even the 4-hour charts that seemed sophisticated enough to work. Daily. The timeframe that requires you to check your screen once per day, make a decision, and then go live your life.

The timeframe that no one on YouTube talks about because it is physically impossible to make a dramatic face while describing it.

Let me introduce you to the five strategies that didn't die.

Strategy #1: GOLD Parabolic SAR D1 with Trailing Stop

Return: +620.49%

Maximum Drawdown: 5.17%

Profit Factor: 3.88

Total Trades: 155

Win Rate: 62.58%

This is the crown jewel. The strategy that made me question everything I thought I knew about trading. And it is absurdly simple.

The Parabolic SAR — Stop and Reverse — is an indicator from the 1970s. Welles Wilder invented it. It puts dots above or below the price to show trend direction. When the dots flip from above to below, you go long. When they flip from below to above, you go short. A child could code it. I am not being hyperbolic; my niece probably could, and she is eleven.

Applied to Gold on the daily chart with a trailing stop exit, this dinosaur of an indicator produced a 620% return over five years with a maximum drawdown of just 5.17%.

Let me put that drawdown number in context. Most hedge funds consider a 20% drawdown "within normal parameters." The S&P 500 dropped 34% in March 2020. My boring, geriatric indicator on the world's most boring timeframe had a max drawdown of 5.17%.

The profit factor of 3.88 means that for every dollar this strategy lost, it made $3.88. Across 155 trades. That is roughly one trade every 6-7 trading days. About three trades per month.

Try making a TikTok about that. "Hey guys, just placed my third trade this month! Now I am going to go read a book and not look at my phone until tomorrow morning!" Zero likes. Zero follows. Zero dopamine hits. Maximum profit.

Strategy #2: GOLD Keltner Channel D1 with Trailing Stop

Return: +341.06%

Maximum Drawdown: 10.61%

Profit Factor: 2.58

Total Trades: 145

The Keltner Channel is essentially Bollinger Bands' less famous cousin. It wraps a moving average with bands based on the Average True Range. When price breaks above the upper band, you buy. When it breaks below the lower band, you sell.

Again, Gold. Again, daily chart. Again, trailing stop. Again, boring as hell. Again, it worked.

341% over five years. The drawdown is higher than the PSAR strategy at 10.61%, which means there were periods where you would be sitting at your desk watching 10% of your account evaporate and wondering if the whole thing was broken. But 145 trades with a profit factor of 2.58 is the kind of result that institutional traders would frame and hang on their wall.

You know what institutional traders would not do? Share it on a Telegram group for $49.99 per month.

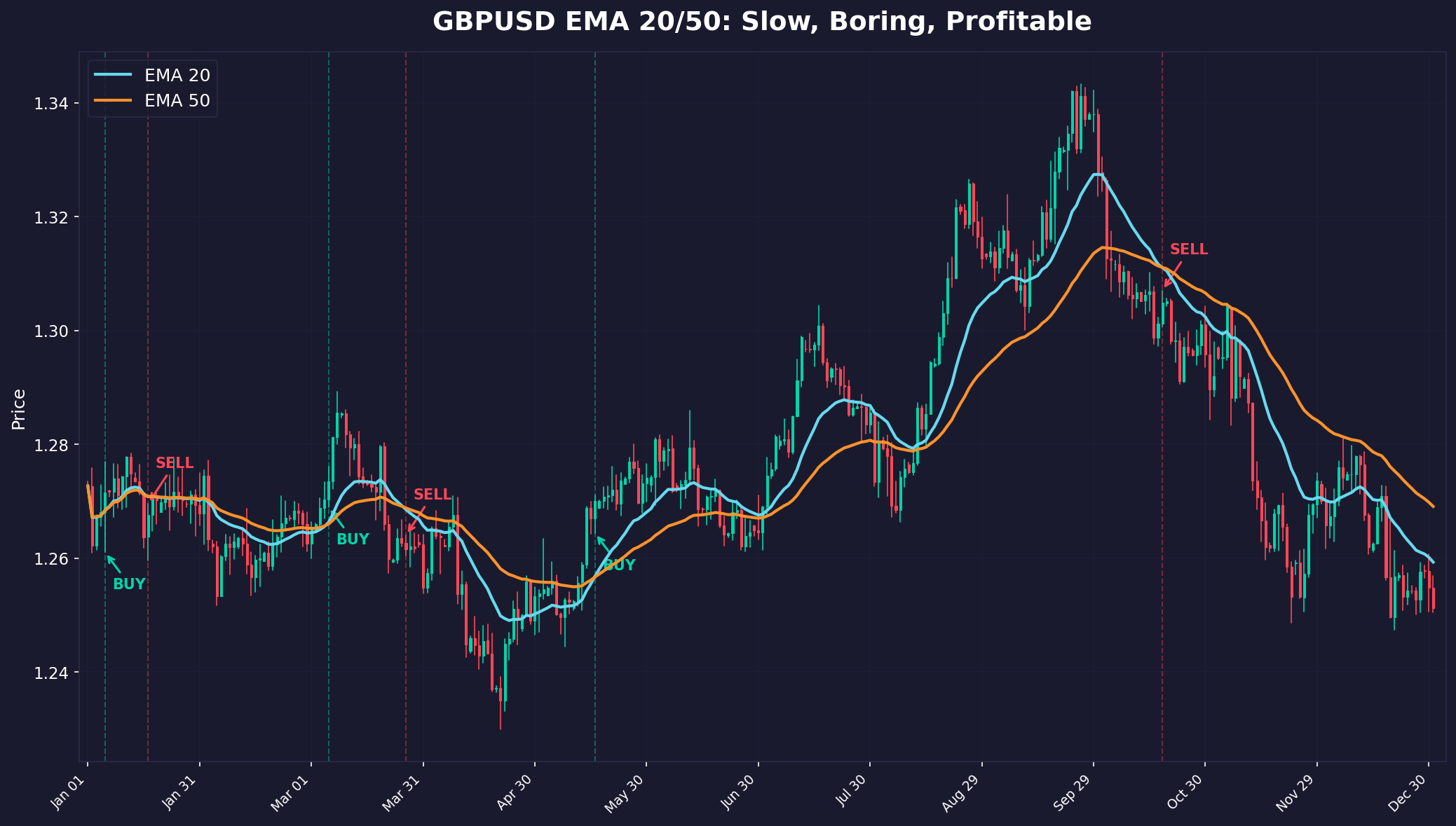

Strategy #3: GBPUSD EMA 20/50 D1 with Opposite Signal Exit

Return: +256.25%

Maximum Drawdown: 29.28%

Profit Factor: 2.04

Total Trades: 31

Win Rate: 51.61%

This one is different. Not Gold. Not a volatility indicator. Just two Exponential Moving Averages — a fast one (20-period) and a slow one (50-period) — applied to the British Pound against the US Dollar.

When the fast EMA crosses above the slow EMA, you go long. When it crosses below, you go short. The exit is not a trailing stop — it is the opposite signal. You stay in the trade until the moving averages cross the other way.

Thirty-one trades in five years. That is roughly one trade every two months. The win rate is barely above a coin flip at 51.61%. But the profit factor of 2.04 tells you the winners were significantly larger than the losers. This strategy wins by catching big trends and riding them until they reverse, not by being right more often than it is wrong.

The drawdown of 29.28% is the highest among our survivors, which makes psychological sense — when you are only taking six trades per year and one goes against you for weeks, your brain starts composing resignation letters to the market. But over five years, those 31 trades turned into a 256% return.

Thirty-one trades. I have seen day traders take 31 trades before lunch.

Strategy #4: DE30 Morning/Evening Star D1

Return: +127.5%

Maximum Drawdown: 21.6%

Profit Factor: 1.83

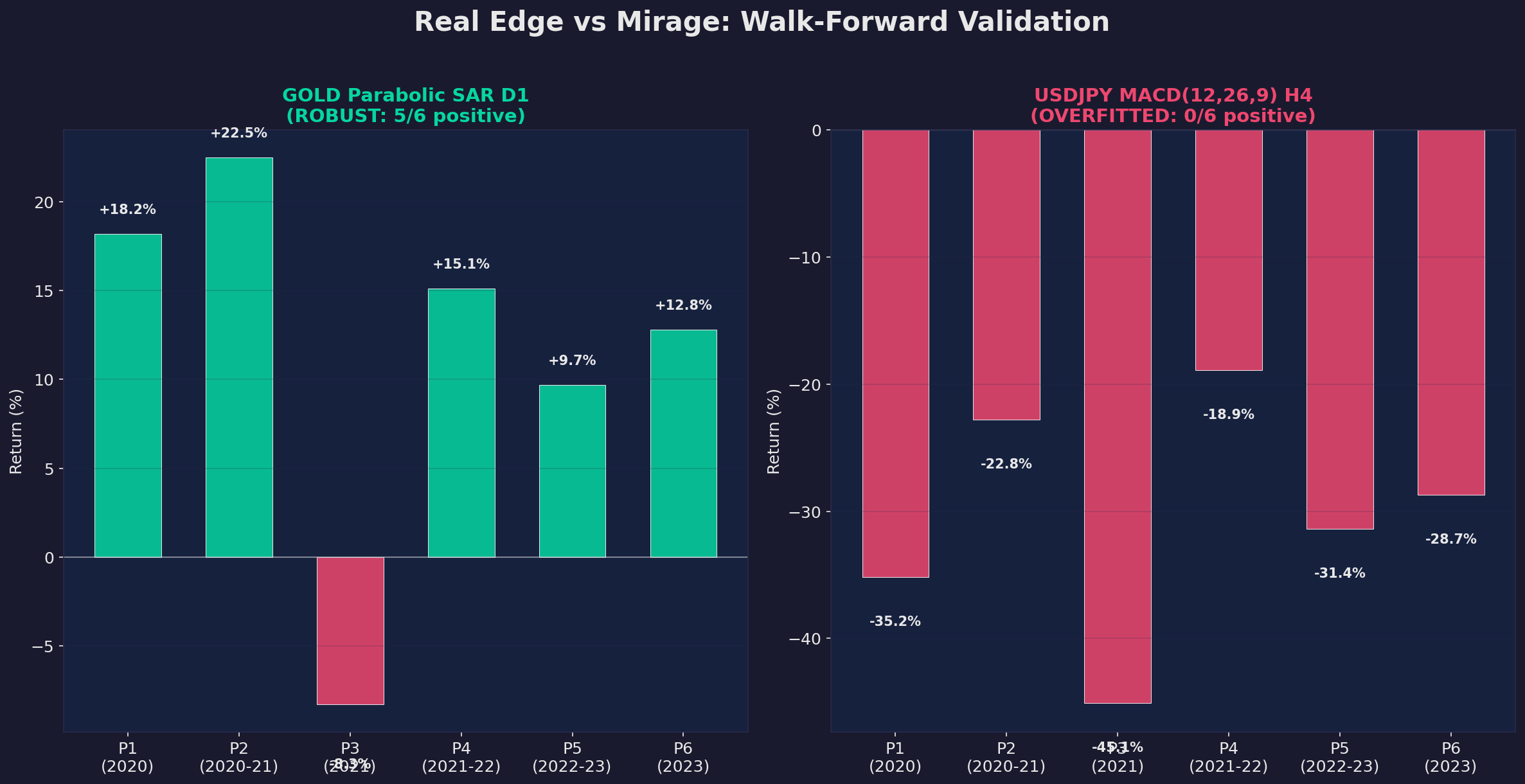

Walk-Forward Validation: 6/6 periods positive — ROBUST

Now we are getting into the more modest returns, and that is perfectly fine because this strategy has something the others need to be jealous of: a perfect walk-forward validation score. Six out of six test periods were profitable. Not five out of six. Not "mostly positive." Six for six. Every single out-of-sample period made money.

The Morning Star and Evening Star are candlestick patterns. They have been around since Japanese rice traders were using them in the 1700s. A Morning Star is a three-candle bullish reversal pattern. An Evening Star is its bearish mirror. Applied to the German DAX index on the daily chart, these patterns from three centuries ago still work.

127.5% over five years will not make anyone's jaw drop. That is roughly 18% per year, which is excellent by any rational standard but will not get you invited to speak at a crypto conference. The profit factor of 1.83 is the lowest among our survivors, meaning the edge is thinner. But it is there. And it survived every single validation period we threw at it.

There is something philosophically satisfying about a pattern from the Edo period outperforming a machine learning algorithm on 1-minute charts. The market has not changed as much as the trading industry wants you to believe.

Strategy #5: EURUSD TRIX D1

Return: +114.2%

Maximum Drawdown: 28.9%

Profit Factor: 1.41

Walk-Forward Validation: 5/6 periods positive — ROBUST

The TRIX indicator is a triple-smoothed exponential moving average shown as a percentage. If that sentence made your eyes glaze over, perfect — you are having the correct reaction. It is a trend-following indicator that filters out noise by smoothing the data three times. It is the trading equivalent of asking someone to repeat themselves three times before you believe them.

Applied to the Euro-Dollar pair on the daily chart, TRIX produced 114.2% over five years. Not spectacular. But robust — five out of six walk-forward periods were positive, meaning this was not a fluke.

The drawdown of 28.9% is substantial. There would have been months where this strategy was deep in the red, and every fiber of your being would scream to turn it off. The people who would have succeeded with this strategy are the people who set it up, verified it was running correctly once per day, and then went to do literally anything else with their lives.

What the Survivors Have in Common

I spent a long time staring at these five strategies, looking for the pattern. Here is what I found:

Daily timeframe. All five. No exceptions. The daily chart filters out the noise, the manipulation, the stop-hunting, the spread widening, the slippage, and all the other micro-level chaos that eats short-timeframe strategies alive.

Patience. The most active strategy (GOLD PSAR) trades about once every six or seven days. The least active (GBPUSD EMA) trades about once every two months. These strategies spend most of their time doing nothing. They wait. They wait some more. Then they act.

Simplicity. A Parabolic SAR. A Keltner Channel. Two moving averages. Candlestick patterns from the 1700s. A triple-smoothed average. None of these are exotic. None require a PhD to understand. None have 15 parameters to optimize. They are the kind of strategies that make quant traders sneer and retail gurus yawn.

Few trades per month. This is the opposite of what the trading industry sells. The industry sells action. Signals. Alerts. Excitement. The market's version of a slot machine, where every ping and notification is another pull of the lever. Our survivors are the anti-slot machine. They are the traders sitting in the corner, reading a newspaper, occasionally glancing at a chart, and quietly making money.

The Trailing Stop Discovery

I need to tell you about the single most important finding of the entire project, and it has nothing to do with entries.

The GOLD Parabolic SAR strategy, before I added the trailing stop, had these stats:

- Return: +150% (approximately)

- Maximum Drawdown: 33%

- Profit Factor: decent but unremarkable

Then I replaced the fixed take-profit with a trailing stop.

- Return: +620.49%

- Maximum Drawdown: 5.17%

- Profit Factor: 3.88

Read those numbers again. The return quadrupled. The drawdown dropped by 85%. The strategy went from "interesting" to "best thing I have ever tested." And I changed exactly one thing: how the strategy exits winning trades.

The fixed take-profit was cutting winning trades at a predetermined level. The trailing stop let winners run, locking in profit as the trade moved in our favor but never capping the upside. When Gold went on a multi-week trend, the fixed TP exited at +2% while the trailing stop rode it to +8%, +12%, sometimes +15%.

The entry was the same. The Parabolic SAR flip. The same signal, the same timing, the same everything — except what happened after you got in.

The exit strategy mattered more than the entry strategy.

I will say it louder for the people in the back who are still arguing about RSI vs. MACD on Twitter: the exit strategy mattered more than the entry strategy.

This finding haunted me. Because the entire retail trading education industry is obsessed with entries. When to get in. What signal to follow. Which indicator is "the best." Every YouTube thumbnail shows an entry arrow. Every course teaches entry techniques. Every Telegram group sends entry signals.

And the thing that actually mattered — what you do after you are in the trade — is barely discussed. It is the afterthought. The boring part. The part that turned a 150% strategy into a 620% strategy.

The Irony

The best trading strategy I found trades about once every 10 days. It requires checking your phone once per day. It is the least exciting thing I have ever built. Instagram would never feature it. No one would pay $99/month for a Telegram channel that sends three signals per month. It has zero content potential. Zero dopamine reward. Zero drama.

And it made +620% in five years.